ARIMA

2017-10-29

Built using Zelig version 5.1.4.90000

++++ All Zelig time series models will be deprecated on 1 February 2018 ++++

Autoregressive and Moving-Average Models with Integration for Time-Series Data

Syntax

z.out <- zarima$new()

z.out$zelig(Y ~ X1 + X2, order = c(1, 0, 0), data = mydata)

x.out$setx(z.out)

s.out$sim(z.out)Additional Inputs

Zelig accepts the following additional inputs for arima to specify variables that provide the time index and any cross-sectional element if there are multiple time-series in the same dataset:

ts: Name of a variable that denotes the time element of the data. As a variable name, this should be in quotes. If this is not provided, Zelig will assume that the data is already ordered by time, but if provided, the dataset will be sorted by this variable before estimation.cs: Name of a variable that denotes the cross-sectional element of the data, for example, country name in a dataset with time-series across different countries. As a variable name, this should be in quotes. If this is not provided, Zelig will assume that all observations come from the same unit over time, and should be pooled, but if provided, individual models will be run in each cross-section. Ifcsis given as an argument,tsmust also be provided.

Examples

Single Series

Attach sample data, which has left party seat share and unemployment across time in several countries. We will subset to just those observations from the United Kingdom:

data(seatshare)

subset <- seatshare[seatshare$country == "UNITED KINGDOM",]Estimate model:

ts.out <- zelig(unemp ~ leftseat, model = 'arima', order = c(1, 0, 1), data = subset)## Warning: ++++ All Zelig time series models will be deprecated on 1 February

## 2018 ++++## How to cite this model in Zelig:

## James Honaker. 2017.

## arima: Autoregressive Moving-Average Models for Time-Series Data

## in Christine Choirat, Christopher Gandrud, James Honaker, Kosuke Imai, Gary King, and Olivia Lau,

## "Zelig: Everyone's Statistical Software," http://zeligproject.org/Summarize estimated model parameters:

summary(ts.out)## Model:

##

## Call:

## z5$zelig(formula = formula, data = data, order = c(1, 0, 1), by = by)

##

## Coefficients:

## ar1 ma1 intercept leftseat

## 0.9028 0.8365 6.5782 -4.0245

## s.e. 0.0606 0.0986 1.9840 1.6622

##

## sigma^2 estimated as 0.527: log likelihood = -44.85, aic = 99.71

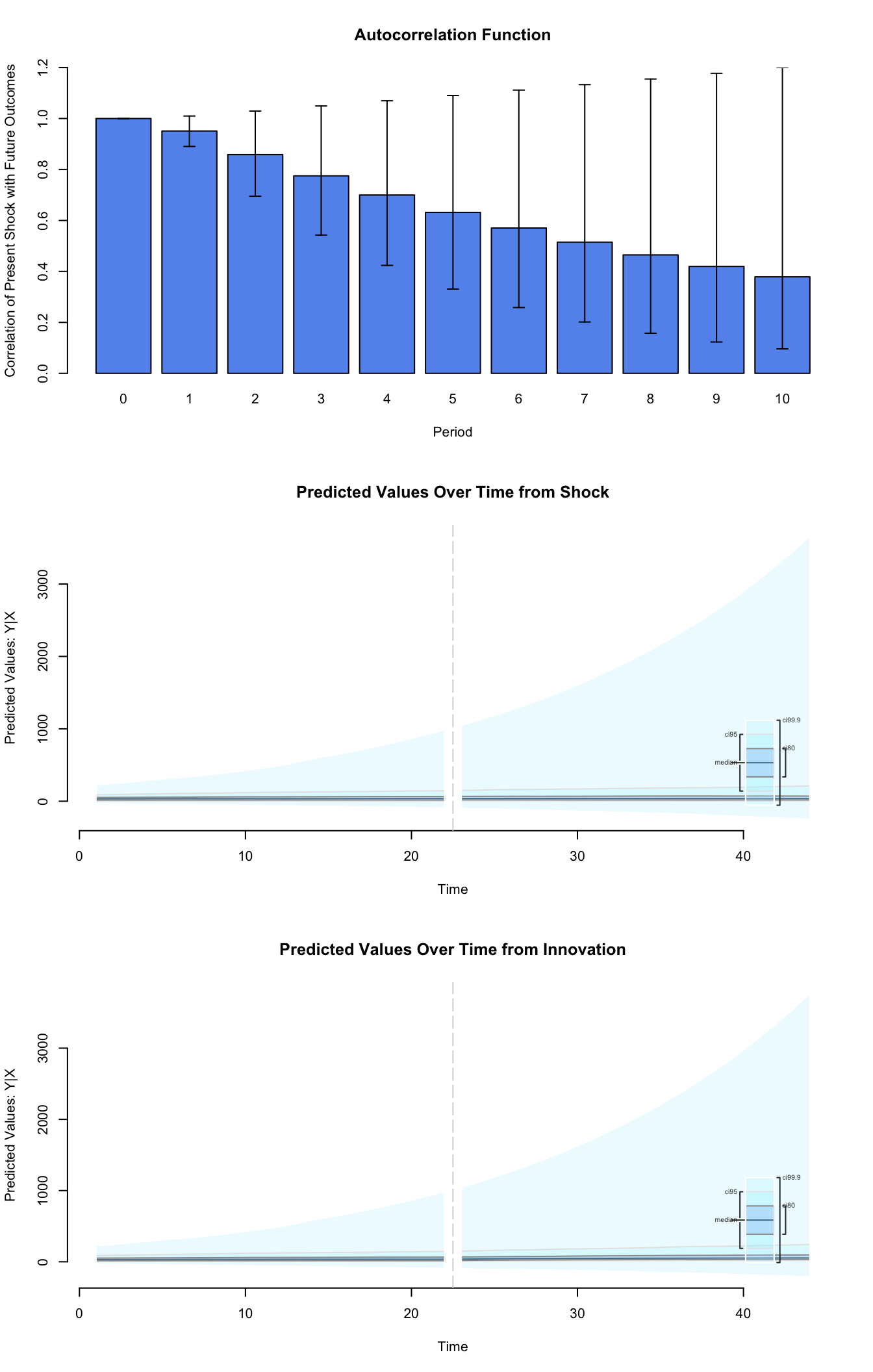

## Next step: Use 'setx' methodNext we simulate what happens when leftseat share drops from a moderately high level of 75 percent, to a rather low level of 25 percent:

## Warning: ++++ All Zelig time series models will be deprecated on 1 February

## 2018 ++++

## Warning: ++++ All Zelig time series models will be deprecated on 1 February

## 2018 ++++

## Warning: ++++ All Zelig time series models will be deprecated on 1 February

## 2018 ++++plot(ts.out)

Graphs of Quantities of Interest for ARIMA models

AR and MA Models

AR (Autoregressive) and MA (Moving Average) models are commonly used in time series analysis. As both AR and MA models are special cases of ARIMA models they are not implemented as separate models within Zelig. Specification of AR and MA models can be accomplished by changing the value of the order parameter within the ARIMA model.

AR

ts.out <- zelig(unemp ~ leftseat, model = "arima", order = c(1, 0, 0), data = subset)MA

ts.out <- zelig(unemp ~ leftseat, model = "arima", order = c(0, 0, 1), data = subset)Multiple Series

The dataset contains similar series for 11 different OECD countries, and we could run the same model on each country’s data. Here we need to specify the ts and cs arguments to identify the names of variables that give the time and cross-section of each observation in the dataset

ts.out2 <- zelig(unemp ~ leftseat, model="arima", order = c(1,0,1), ts = "year",

cs = "country", data = seatshare)## Warning: ++++ All Zelig time series models will be deprecated on 1 February

## 2018 ++++## How to cite this model in Zelig:

## James Honaker. 2017.

## arima: Autoregressive Moving-Average Models for Time-Series Data

## in Christine Choirat, Christopher Gandrud, James Honaker, Kosuke Imai, Gary King, and Olivia Lau,

## "Zelig: Everyone's Statistical Software," http://zeligproject.org/summary(ts.out2)## Model:

## $country

## [1] "AUSTRALIA"

##

##

## Call:

## z5$zelig(formula = unemp ~ leftseat, data = seatshare, order = c(1, 0, 1), ts = "year",

## cs = "country")

##

## Coefficients:

## ar1 ma1 intercept leftseat

## 0.8849 0.5030 5.5878 0.5572

## s.e. 0.0807 0.1693 1.9419 2.0036

##

## sigma^2 estimated as 0.8582: log likelihood = -44.24, aic = 98.47

## Model:

## $country

## [1] "AUSTRIA"

##

##

## Call:

## z5$zelig(formula = unemp ~ leftseat, data = seatshare, order = c(1, 0, 1), ts = "year",

## cs = "country")

##

## Coefficients:

## ar1 ma1 intercept leftseat

## 0.9553 0.7052 4.0325 1.5252

## s.e. 0.0395 0.1912 2.9062 5.3451

##

## sigma^2 estimated as 0.1231: log likelihood = -16.57, aic = 43.14

## Model:

## $country

## [1] "CANADA"

##

##

## Call:

## z5$zelig(formula = unemp ~ leftseat, data = seatshare, order = c(1, 0, 1), ts = "year",

## cs = "country")

##

## Coefficients:

## ar1 ma1 intercept leftseat

## 0.8433 0.4100 7.7866 -0.3316

## s.e. 0.0819 0.1538 1.3222 1.4821

##

## sigma^2 estimated as 0.7389: log likelihood = -50.45, aic = 110.89

## Model:

## $country

## [1] "FINLAND"

##

##

## Call:

## z5$zelig(formula = unemp ~ leftseat, data = seatshare, order = c(1, 0, 1), ts = "year",

## cs = "country")

##

## Coefficients:

## ar1 ma1 intercept leftseat

## 0.924 0.4631 -11.5415 21.2130

## s.e. 0.057 0.1089 8.8316 10.1507

##

## sigma^2 estimated as 1.656: log likelihood = -66.61, aic = 143.23

## Model:

## $country

## [1] "FRANCE"

##

##

## Call:

## z5$zelig(formula = unemp ~ leftseat, data = seatshare, order = c(1, 0, 1), ts = "year",

## cs = "country")

##

## Coefficients:

## ar1 ma1 intercept leftseat

## 0.9850 0.4634 6.7010 -0.5321

## s.e. 0.0189 0.1666 4.1873 0.8049

##

## sigma^2 estimated as 0.3057: log likelihood = -31.18, aic = 72.36

## Model:

## $country

## [1] "ITALY"

##

##

## Call:

## z5$zelig(formula = unemp ~ leftseat, data = seatshare, order = c(1, 0, 1), ts = "year",

## cs = "country")

##

## Coefficients:

## ar1 ma1 intercept leftseat

## 0.9613 0.5843 10.4435 -4.3455

## s.e. 0.0370 0.1384 2.5518 3.3636

##

## sigma^2 estimated as 0.2537: log likelihood = -30.54, aic = 71.07

## Model:

## $country

## [1] "NORWAY"

##

##

## Call:

## z5$zelig(formula = unemp ~ leftseat, data = seatshare, order = c(1, 0, 1), ts = "year",

## cs = "country")

##

## Coefficients:

## ar1 ma1 intercept leftseat

## 0.8572 0.5438 5.4875 -5.3044

## s.e. 0.0890 0.1484 3.2045 6.3460

##

## sigma^2 estimated as 0.2459: log likelihood = -20.6, aic = 51.19

## Model:

## $country

## [1] "SPAIN"

##

##

## Call:

## z5$zelig(formula = unemp ~ leftseat, data = seatshare, order = c(1, 0, 1), ts = "year",

## cs = "country")

##

## Coefficients:

## ar1 ma1 intercept leftseat

## 0.9496 0.9999 12.9842 0.7673

## s.e. 0.0537 0.1213 5.9394 3.7856

##

## sigma^2 estimated as 1.179: log likelihood = -36.4, aic = 82.8

## Model:

## $country

## [1] "SWEDEN"

##

##

## Call:

## z5$zelig(formula = unemp ~ leftseat, data = seatshare, order = c(1, 0, 1), ts = "year",

## cs = "country")

##

## Coefficients:

## ar1 ma1 intercept leftseat

## 0.8303 1.0000 9.2331 -9.6728

## s.e. 0.0843 0.0849 1.4452 1.7366

##

## sigma^2 estimated as 0.2909: log likelihood = -32.65, aic = 75.31

## Model:

## $country

## [1] "UNITED KINGDOM"

##

##

## Call:

## z5$zelig(formula = unemp ~ leftseat, data = seatshare, order = c(1, 0, 1), ts = "year",

## cs = "country")

##

## Coefficients:

## ar1 ma1 intercept leftseat

## 0.9028 0.8365 6.5782 -4.0245

## s.e. 0.0606 0.0986 1.9840 1.6622

##

## sigma^2 estimated as 0.527: log likelihood = -44.85, aic = 99.71

## Model:

## $country

## [1] "UNITED STATES"

##

##

## Call:

## z5$zelig(formula = unemp ~ leftseat, data = seatshare, order = c(1, 0, 1), ts = "year",

## cs = "country")

##

## Coefficients:

## ar1 ma1 intercept leftseat

## 0.6518 0.3493 3.8765 3.6727

## s.e. 0.1586 0.2534 2.6929 4.4801

##

## sigma^2 estimated as 0.7245: log likelihood = -45.83, aic = 101.66

## Next step: Use 'setx' methodSee Also

The estimator used for ARIMA models is part of the stats package by William N. Venables and Brian D. Ripley .In addition, advanced users may wish to refer to help(arima).

## Warning: ++++ All Zelig time series models will be deprecated on 1 February

## 2018 ++++R Core Team (2017). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria. <URL: https://www.R-project.org/>.